1QFY2017 Result Update | Financial

August 1, 2016

Equitas Holdings

BUY

CMP

`195

Performance Highlights

Target Price

`235

Investment Period

12 months

Particulars (` cr)

1QFY17 4QFY16

% chg (qoq) 1QFY16

% chg (yoy)

NII

190.3

162.9

16.9

125.6

51.6

Pre-prov. profit

113.9

87.5

30.1

74.5

52.8

Stock Info

PAT

61.2

46.8

30.7

37.4

63.6

Sector

Financial

Source: Company, Angel Research

Market Cap (` cr)

6,554

Equitas Holdings (Equitas) reported a strong set of results for 1QFY2017. Its AUM

Beta

0.9

grew by 48% yoy which led to a PAT growth of 64% yoy to `61cr, both beating

52 Week High / Low

206 / 134

our expectations. The Management remains confident of sustenance of business growth in

the years to come and expects to start the small finance bank (SFB) by 2QFY2017 end.

Avg. Daily Volume

883,000

AUM growth remained strong, on track to start SFB: The company’s AUM for the

Face Value (`)

10

quarter grew by 48.4% yoy/7.1% qoq to `6,559cr. The MFI, (Vehicle Finance +

BSE Sensex

28,052

MSE), and the Home Finance segments grew by 48%, 50%, and 32% yoy

Nifty

8,638

respectively. We believe the company will be able to achieve similar growth in the

Reuters Code

NA

quarters to come. With the start of the SFB operations, Equitas will also offer

Agriculture Gold Loans and Business Loans which will enable it to meet the

Bloomberg Code

EQUITAS.IN

priority sector lending norm. The AUM mix remained stable.

Rise in NPAs due to migration to 120 days NPA recognition norm from 150 days:

The 27bp sequential rise in GNPAs to 1.61% during the quarter is largely due to

Shareholding Pattern (%)

the company’s migration to 4-months NPA recognition norm from 5 months

Promoters

0.0

earlier. Given that the company intends to start its banking operations by

MF / Banks / Indian Fls

26.9

2QFY2017 end, it will then have to move to the 3-months NPA recognition norm,

FII / NRIs / OCBs

48.5

which could lead to further escalation in NPAs in 2QFY2017. However, from an

operational point of view, the asset quality has not deteriorated, as on a like to

Indian Public / Others

24.6

like basis, the rise in GNPAs for 1QFY2017 would have been of 5-10bp only.

Margins to moderate down: The reported NIM for the quarter has improved to

12% vs 11.92% in 1QFY2016 and vs 11.40% for the entire FY2016 period.

Abs.(%)

3m

1yr

3yr

However, post the initiation of SFB operations, the maintenance of SLR and CRR

Sensex

9.5

1.8

43.2

will impact NIM to some extent. While the new bank will have access to lower cost

Equitas

43.1

NA NA

funds it will take time to get sizeable access to the low cost CASA.

Outlook and valuation: We continue to believe that Equitas is strongly positioned

3-Year Daily Price Chart

to grow on the back of its balanced portfolio. Conversion to a SFB will have its

220

own challenges. However, the market segment which the upcoming bank intends

200

to cater to has vast untapped business potential and exploiting it effectively will

180

drive the company’s growth for multiple years. Despite costs having to be incurred

160

in order to meet regulatory requirements (SLR + SRR), we believe the company

140

will be able to deliver a ROA of 2.5% and ROE of 11.5% by FY2018. At the

120

current market price the stock is trading at 2.3x its FY2018E BV of `75.6. We

100

maintain BUY on the stock with a target price of `235.

Key Financials (Consolidated)

Y/E March (` cr)

FY2015

FY2016

FY2017E

FY2018E

Source: Company, Angel Research

Operating Income

460

675

934

1,274

% chg

57.2

46.6

38.4

36.4

Net profit

106.6

167.1

195.6

275.9

% chg

44.0

56.2

17.1

41.0

NIM (%)

12.9

12.4

11.7

11.5

EPS (`)

4.0

6.2

5.8

8.2

P/E (x)

49.0

31.5

33.4

23.7

P/ABV (x)

4.1

3.0

2.7

Siddharth Purohit

RoA (%)

3.0

3.1

2.5

2.5

022 - 3935 7800 Ext: 6872

RoE (%)

11.2

13.3

10.9

11.5

Source: Company, Angel Research; Note: CMP as of July 29, 2016

Please refer to important disclosures at the end of this report

1

Equitas Holdings | 1QFY2017 Result Update

Exhibit 1: 1QFY2017 performance (standalone)

Particulars (` cr)

1QFY17

4QFY16

% chg (qoq)

1QFY16

% chg (yoy)

FY2016

FY2015

% chg

Net interest income

190.3

162.9

16.9

125.6

51.6

577.7

392.1

47.3

Non-interest income

37.0

29.6

24.8

23.74

55.8

101.2

69.1

46.4

Operating income

227.3

192.5

18.1

149.3

52.2

678.9

461.2

47.2

Operating expenses

113.4

105.0

8.0

74.8

51.7

359.7

247.2

45.5

Pre-prov. profit

113.9

87.5

30.1

74.5

52.8

319.2

214.0

49.2

Provisions & cont.

17.6

14.6

20.3

16.5

6.7

59.1

50.4

17.2

PBT

96.3

72.9

32.1

58.1

65.8

260.1

163.6

59.0

Prov. for taxes

35.2

26.1

34.6

20.7

69.8

93.0

57.0

63.3

PAT

61.2

46.8

30.7

37.4

63.6

167.1

106.6

56.2

EPS (`)

1.8

1.4

30.7

1.4

31.1

6.2

4.0

55.0

Cost-to-income ratio (%)

49.9

54.5

50.1

53.0

53.6

Effective tax rate (%)

36.5

35.8

35.7

35.7

34.8

Source: Company, Angel Research

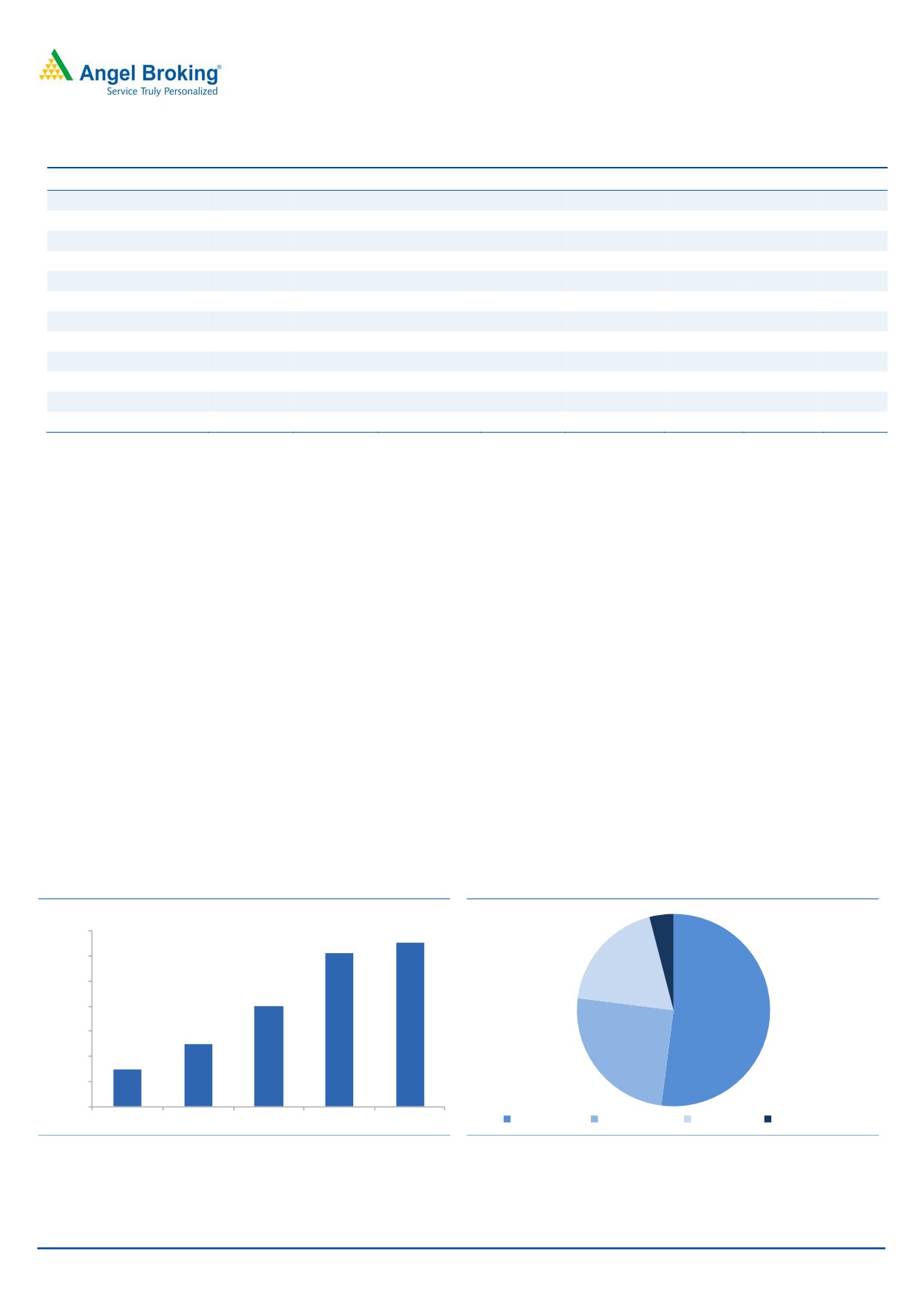

AUM growth remained strong and likely to remain robust going ahead: During the

quarter, Equitas continued to report strong growth in its AUM, which is of 48.4%

yoy / 7.1% qoq. A close look at the segmental performance shows that the growth

has been secular across verticals with the Vehicle Finance + MSE segment

reporting the highest growth of 50% yoy / 10% qoq. The Microfinance business also

grew by a strong 48.4% yoy / 4.8% qoq. The growth was in spite the Tamil Nadu

elections in May 2016 and a severe heat wave hitting the state. With a good monsoon,

we expect growth to pick up further. Though the Management has remained selective

in the Home Finance segment, it has still been able to report a 32% yoy / 4.5% qoq

growth in the segment during the quarter.

AUM mix remains healthy with a bias in favor of non-Microfinance loans: The

Management has been able to grow the balance sheet with a primary focus on the

microfinance segment while the Vehicle Finance + MSE segment also supported

growth. Further, to complement the operations of the upcoming SFB, the

Management intends to start two new products, (a) Agriculture Gold Loans and (b)

Business Loans, which will help the bank in meeting the priority sector lending

norm. The overall AUM mix remained stable.

Exhibit 2: AUM growth remains strong

Exhibit 3: Loan Mix

(` cr)

7,000

6,558

4%

6,125

6,000

19%

5,000

4,010

4,000

52%

3,000

2,486

2,000

1,485

25%

1,000

-

FY13

FY14

FY15

FY16

1QFY17

Micro Finance

Vehicle Finance

MSE Finance

Housing Finance

Source: Company, Angel Research

Source: Company, Angel Research

August 1, 2016

2

Equitas Holdings | 1QFY2017 Result Update

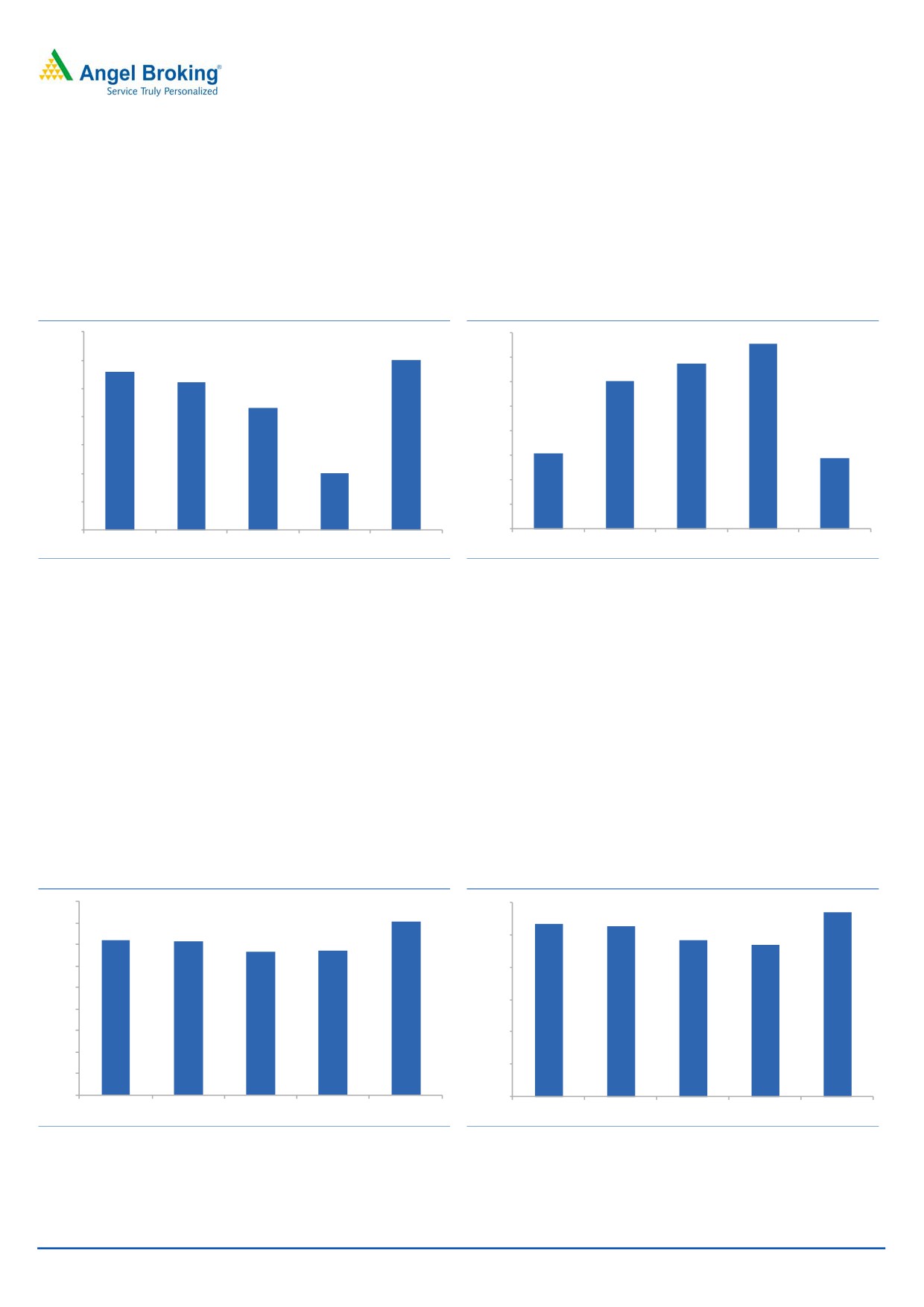

Margins to see moderation: The reported NIM has improved to 12% vs 11.92% in

1QFY2016 and vs 11.40% for the entire year FY2016. However, going forward,

the NIM could take some adverse impact post the conversion to a SFB wherein SLR

and CRR maintenance norms will have to be adhered to. While the new bank will

have access to lower cost funds it will take time to get sizeable access to the low

cost CASA.

Exhibit 4: NIM to see moderation going ahead

Exhibit 5: Cost to Income trend

12.2%

55.0%

54.5%

12.0%

53.7%

12.0%

11.9%

54.0%

11.8%

53.0%

53.0%

11.8%

11.7%

52.0%

11.6%

51.0%

50.1%

11.4%

49.9%

50.0%

11.2%

11.2%

49.0%

11.0%

48.0%

10.8%

47.0%

1QFY16

2QFY16

3QFY16

4QFY16

1QFY17

1QFY16

2QFY16

3QFY16

4QFY16

1QFY17

Source: Company, Angel Research

Source: Company, Angel Research

Asset quality marginally weakened due to migration to NPA recognition at 4

months compared to 5 months earlier: Equitas has so far been able to maintain its

asset quality. The 27bp sequential rise in GNPAs to 1.61% during the quarter is

largely due to the company’s migration to 4-months NPA recognition norm from 5

months earlier. So a large part of the rise in NPA can be attributed to the change

in regulatory compliance norms which the company will have to fall in line with

before starting banking operations. Hence there could be a further rise in NPAs in

2QFY2017. However, without the migration effect, the rise in GNPAs would only

have been of 5-10bp, which indicates at there being no weakness in asset quality

during the quarter. The Management has indicated that with the compliance to the

90-days NPA recognition norm, GNPAs could rise to 2.20%.

Exhibit 6: Rise in GNPAs due to regulatory adherence

Exhibit 7: Trend in Net NPA

1.8%

1.20%

1.14%

1.61%

1.07%

1.05%

1.6%

1.4%

1.4%

0.97%

1.00%

0.94%

1.3%

1.3%

1.4%

1.2%

0.80%

1.0%

0.60%

0.8%

0.6%

0.40%

0.4%

0.20%

0.2%

0.0%

0.00%

1QFY16

2QFY16

3QFY16

4QFY16

1QFY17

1QFY16

2QFY16

3QFY16

4QFY16

1QFY17

Source: Company, Angel Research

Source: Company, Angel Research

August 1, 2016

3

Equitas Holdings | 1QFY2017 Result Update

Exhibit 8: Key Operating Parameters

AUM (` Cr)

FY13

FY14

FY15

FY16

Q1FY16

Q4FY16

Q1FY17

YOY%

% QoQ

EMFL

1,135

1,503

2,144

3,283

2,319

3,283

3,442

48.4

4.8

EFL

305

889

1,686

2,596

1,905

2,596

2,859

50.1

10.1

EHFL

45

94

180

246

195

246

257

31.8

4.5

Total

1,485

2,486

4,010

6,125

4,419

6,125

6,558

48.4

7.1

Disbursments (` Cr)

EMFL

1,149

1,505

2,129

3,173

620

931

802

29.4

(13.9)

EFL

300

818

1,365

1,917

413

564

565

36.8

0

EHFL

21

29

24

14.3

(14.3)

Total

1,449

2,323

3,494

5,090

1,054

1,524

1,391

32.0

(8.7)

As % of AUM

EMFL

76.4

60.5

53.5

53.6

52.5

53.6

52.5

EFL

20.5

35.8

42.0

42.4

43.1

42.4

43.6

EHFL

3.0

3.8

4.5

4.0

4.4

4.0

3.9

Source: Company, Angel Research

Exhibit 9: Segmental NPA%

Gross NPAs %

FY13

FY14

FY15

FY16

Q1FY16

Q4FY16

Q1FY17

Microfinance Business

0.00

0.10

0.10

0.23

0.11

0.23

0.25

Non Micro Finance Business

1.00

1.60

2.00

2.49

2.67

2.49

3.03

Net NPAs %

Micro Finance Business

0.00

0.00

0.00

0.06

0.04

0.06

0.05

Non Micro Finance Business

0.70

1.40

1.50

2.49

2.67

2.49

3.03

Consolidated GNPAs %

0.30

0.70

1.08

1.34

1.44

1.34

1.61

Consolidated NNPAs %

0.20

0.60

0.80

0.94

1.07

0.94

1.14

Credit Cost %

0.77

0.93

1.55

1.17

1.56

1.17

1.11

Source: Company, Angel Research

Outlook and valuation

We continue to believe that Equitas is strongly positioned to grow on the back of its

balanced portfolio. Conversion to a SFB will have its own challenges. However, the

market segment which the upcoming bank intends to cater to has vast untapped

business potential and exploiting it effectively will drive the company’s growth for

multiple years. Despite costs having to be incurred in order to meet regulatory

requirements (SLR + SRR), we believe the company will be able to deliver a ROA of

2.5% and ROE of 11.5% by FY2018. At the current market price the stock is

trading at 2.3x its FY2018E BV of `75.6. We maintain BUY on the stock with a

target price of `235.

August 1, 2016

4

Equitas Holdings | 1QFY2017 Result Update

Company Background

Equitas is a diversified financial services player with strong presence across

microfinance, vehicle finance, MSE finance, and housing finance segments.

Incorporated in 2007 and headquartered in Chennai, Equitas operates across 11

states through 549 branches. Equitas, through its subsidiary Equitas Micro Finance

Ltd (EMFL) is the fifth largest microfinance company in India (on gross loan

portfolio basis). Equitas has also received in-principle approval from the RBI to set

up a SFB in October 2015.

Key Management Personnel:

P. N. Vasudevan, Managing Director.

S. Bhaskar, CFO, joined the Equitas Group in 2007.

H.K.N. Raghavan, CEO of EMFL, joined the Equitas Group in 2008.

V. S. Murthy, CEO of Equitas Finance Ltd (EFL), joined the Equitas Group in 2010.

August 1, 2016

5

Equitas Holdings | 1QFY2017 Result Update

Income statement (standalone)

Y/E March (` cr)

FY2014

FY2015

FY2016

FY2017E

FY2018E

NII

293

460

675

934

1,274

- YoY Growth (%)

67.8

57.2

46.6

38.4

36.4

Other Income

1.1

0.9

3.9

5.1

6.9

- YoY Growth (%)

-

-

-

30.5

35.0

Operating Income

294.0

461.2

678.9

939.2

1280.8

- YoY Growth (%)

67.5

56.9

47.2

38.3

36.4

Operating Expenses

161.8

247.2

359.7

535.4

730.1

- YoY Growth (%)

28.4

52.8

45.5

48.8

36.4

Pre - Provision Profit

132.2

214.0

319.2

403.9

550.7

- YoY Growth (%)

166.9

61.9

49.2

26.5

36.4

Prov. & Cont.

18.4

50.4

59.1

102.9

138.9

- YoY Growth (%)

106.5

174.1

17.2

74.1

35.0

Profit Before Tax

113.8

163.6

260.1

301.0

411.8

- YoY Growth (%)

186.3

43.7

59.0

15.7

36.8

Prov. for Taxation

39.5

56.6

93.0

105.3

135.9

- as a % of PBT

35

35

36

35

33

PAT

74.3

107.0

167.1

195.6

275.9

- YoY Growth (%)

133.0

44.0

56.2

17.1

41.0

Balance sheet (standalone)

Y/E March (` cr)

FY2014 FY2015 FY2016

FY2017E

FY2018E

Share Capital

73

269

270

335

335

Reserve & Surplus

669

902

1,071

1,921

2,197

Net Worth

742

1,172

1,341

2,256

2,532

Borrowings

1,849

3,032

4,683

6,557

7,868

- Growth (%)

45

64

54

40

20

Deposits

-

-

-

350

1,850

- Growth (%)

-

-

-

-

429

Other Liab. & Prov.

160

262

482

426

575

Total Liabilities

2,751

4,466

6,507

9,588

12,825

Cash and Cash Equivalents

415

557

947

852

958

Investments

72

176

12

1,468

1,731

Advances

2,123

3,465

5,070

7,098

9,583

- Growth (%)

75

63

46

40

35

Fixed Assets

27

47

66

86

111

Other Assets

114

222

412

85

442

Total Assets

2,751

4,466

6,507

9,588

12,825

August 1, 2016

6

Equitas Holdings | 1QFY2017 Result Update

Ratio analysis (standalone)

Y/E March

FY2014

FY2015

FY2016

FY2017E

FY2018E

Profitability ratios (%)

NIMs

12.9

12.9

12.4

11.7

11.5

RoA

3.3

3.0

3.1

2.5

2.5

RoE

12.2

11.2

13.3

10.9

11.5

Asset Quality (%)

Gross NPAs

15.5

37.4

68.1

140.3

188.4

Gross NPAs %

0.7

1.1

1.3

1.6

1.6

Net NPAs

13.0

27.8

47.8

87.0

116.8

Net NPAs %

0.6

0.8

0.9

1.0

1.0

Credit Cost

0.9

1.5

1.2

1.2

1.2

Per Share Data (`)

EPS

10.2

4.0

6.2

5.8

8.2

BVPS

102.1

43.6

49.7

67.4

75.6

Adj BV

100.3

42.5

47.9

64.8

72.1

Valuation Ratios

PER (x)

19.1

49.0

31.5

33.4

23.7

P/ABVPS (x)

NA

NA

4.1

3.0

2.7

Dividend Yield (%)

-

-

-

-

-

DuPont Analysis

Interest Income

21.0

20.9

20.2

19.3

18.4

Interest Expenses

8.2

8.2

7.9

7.7

7.1

NII

12.7

12.8

12.3

11.6

11.4

(-) Prov. Exp.

0.0

0.0

0.1

0.1

0.1

Adj. NII

12.8

12.8

12.4

11.7

11.4

Other Inc.

7.0

6.9

6.6

6.7

6.5

Op. Inc.

5.7

5.9

5.8

5.0

4.9

Opex

0.8

1.4

1.1

1.3

1.2

PBT

4.9

4.5

4.7

3.7

3.7

Taxes

1.7

1.6

1.7

1.3

1.2

RoA

3.2

3.0

3.0

2.4

2.5

Leverage

3.8

3.8

4.4

4.5

4.7

RoE

12.2

11.2

13.3

10.9

11.5

August 1, 2016

7

Equitas Holdings | 1QFY2017 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with CDSL

and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or co-managed public

offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Disclosure of Interest Statement

Equitas Holdings

1. Financial interest of research analyst or Angel or his Associate or his relative

No

2. Ownership of 1% or more of the stock by research analyst or Angel or associates or relatives

No

3. Served as an officer, director or employee of the company covered under Research

No

4. Broking relationship with company covered under Research

No

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

August 1, 2016

8